Life has a way of throwing curveballs when you least expect it. One minute, you’re cruising down a California highway, maybe humming along to your favorite tune. The next, a distracted driver slams into you, and suddenly, you’re sidelined with an injury, unable to work. Your paycheck? Gone AWOL. Your savings? Taking a nosedive.

If this sounds like your story, I feel you, and I’m here to help. Welcome to your go-to guide on loss of wages, loss of earnings, and how to fight for wage loss compensation in the Golden State. We’ll dig into what loss of income insurance provides, explore the ins and outs of suing for loss of potential income, and show you how to build a killer loss of earnings claim. With Joseph Pluta Law At Attorney in your corner, you’ve got a shot at turning this mess around. Let’s dive in.

The Hidden Cost of an Injury

An injury doesn’t just bruise your body—it bruises your bank account. Loss of wages is the money you’re missing out on because you can’t clock in. Maybe you’re a barista, a teacher, or a freelancer, and those paychecks you counted on have vanished. Loss of earnings takes it a step further, covering both the cash you’ve already lost and the future income that might slip through your fingers. In California, where rent can eat half your income and bills stack up faster than traffic on the 405, this stuff matters.

Let me tell you about Maria, a barista in San Diego. She slipped on a wet floor at work, sprained her wrist, and couldn’t pour lattes for three months. That meant $2,500 a month in wages lost—$7,500 total. Her rent didn’t pause, and neither did her stress. That’s why understanding wage loss compensation is a game-changer. Stick with me, and we’ll walk through how to get what you’re owed.

Breaking Down Your Loss of Earnings

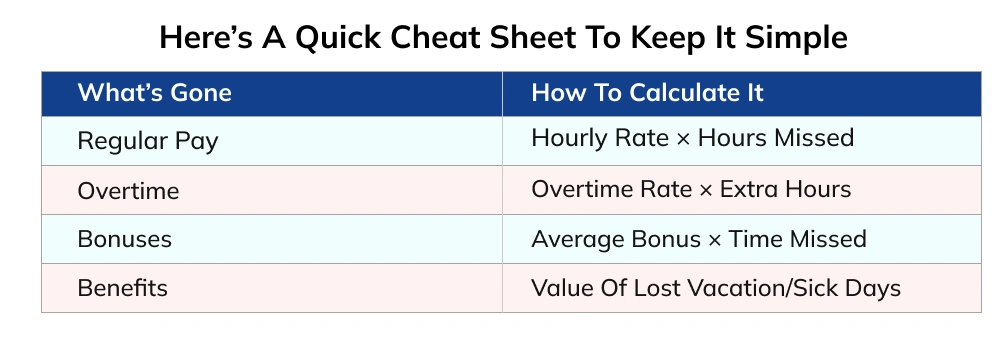

So, how much are you really out? Calculating your loss of earnings is like piecing together a puzzle, but don’t worry—it’s not as hard as it sounds. Let’s break it down.

First, look at what you’ve already missed. Say you’re a construction worker earning $30 an hour. You’re out for 160 hours (a month of full-time work). That’s $4,800 in loss of wages. But it’s not just your base pay. Did you miss out on overtime? A holiday bonus? Those unused vacation days? Add those in. For example, if you normally get $500 in overtime and a $200 bonus, that’s another $700 gone.

Now, think long-term. If your injury keeps you from working for months—or changes your job altogether—you need to factor in future losses. A nurse missing six months at $5,000 a month? That’s $30,000. If you can’t return to your old role, your loss of earnings claim needs to account for that too.

Gig Workers, Listen Up: If you’re a freelancer or drive for Uber, proving loss of earnings can be trickier. Grab your 1099s, invoices, or PayPal records. For example, my friend Jake, a rideshare driver, used his trip logs to show he was earning $3,000 a month before a crash. That proof helped him claim his wages lost. Want to make this easy? Download our free “Wage Loss Checklist” at the end of this post to stay organized.

Decoding Loss of Income Insurance

You might be thinking, “I’ve got loss of income insurance—I’m golden, right?” Not so fast. Let’s unpack what loss of income insurance provides and where it might leave you hanging.

This type of insurance is supposed to kick in when an injury stops your paycheck. Sounds like a lifesaver, but policies are sneaky. Some might cover 70% of your salary for three months; others cap you at $1,500 a month, even if you earn double that. And don’t get me started on the fine print—some exclude bonuses, overtime, or even certain injuries.

Take Lisa, a graphic designer in LA. Her loss of income insurance paid $2,000 a month, but her actual loss of wages was $4,000. She had to file a loss of earnings claim to cover the gap. Another gotcha? Waiting periods. Some policies make you wait 30 days before paying out, leaving you to scrape by in the meantime.

Here’s your action plan: Pull out your policy and read it like it’s a treasure map. Look for caps, exclusions, and how long it covers. Confused? You’re not alone. A quick chat with a pro can clear things up and make sure you’re not shortchanged.

When an Injury Steals Your Future

Loss of earning potential is the gut-punch you don’t see coming. It’s not just about the wages lost today—it’s the career you were building for tomorrow. Maybe you’re a roofer who can’t climb ladders anymore or a teacher stuck on desk duty because of back pain. That’s where suing for loss of potential income comes in.

Picture Sarah, a 32-year-old nurse in Sacramento. She was on track to become a head nurse, pulling in $80,000 a year. A car accident left her with chronic pain, limiting her to part-time work at $40,000 a year. Over 20 years, that’s $800,000 in lost earnings. That’s what loss of potential income means.

Proving this isn’t easy—you might need a vocational expert to show how your career’s been derailed or an economist to crunch the numbers. This is where having a sharp legal team makes all the difference.

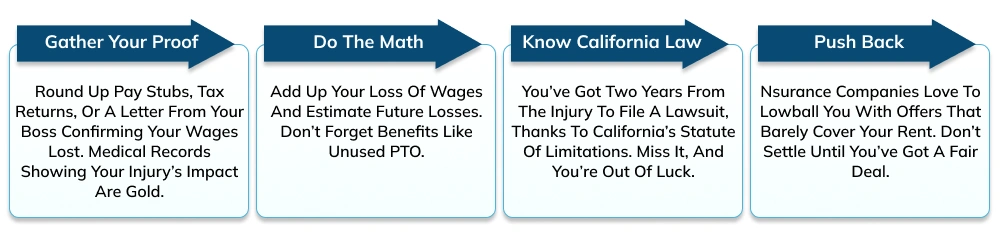

Building a Winning Case for Compensation

Ready to fight for what’s yours? Whether you’re chasing wage loss compensation or suing for loss of potential income, a strong loss of earnings claim is your ticket. Here’s how to make it happen:

My cousin Tom, a roofer in Fresno, learned this the hard way. A fall left him unable to work, costing him $30,000 in loss of wages. Worse, he couldn’t return to roofing, slashing his future earnings. With Joseph Pluta Law At Attorney, he built a solid loss of earnings claim, landing $30,000 for past losses and $100,000 for loss of potential income. Their team brought in experts and fought the insurance company’s nonsense, proving Tom’s case.

A good lawyer can make or break your claim. They’ll handle the paperwork, negotiate with insurance sharks, and make sure you don’t settle for pennies.

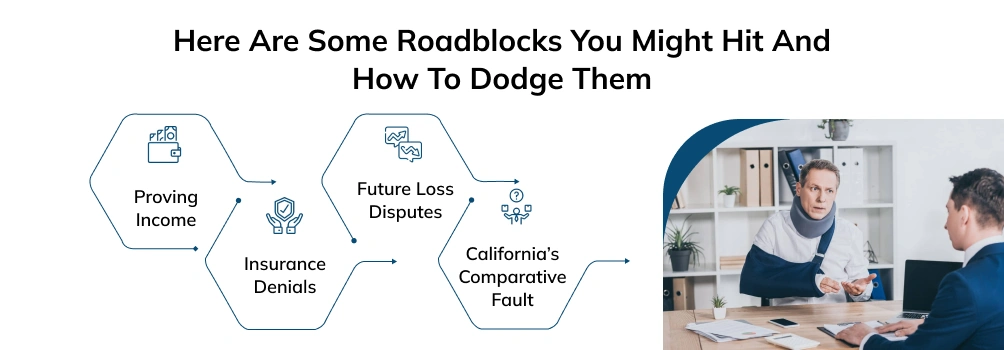

How To Avoid Common Pitfalls While Receiving Wage Compensation

Nobody said getting wage loss compensation was a walk in the park. Here are some roadblocks you might hit and how to dodge them:

- Proving Income: If you’re a freelancer or gig worker, showing loss of earnings can be tough. Use tax returns, invoices, or even Venmo records. Lisa, a freelance writer, got denied because her income wasn’t “steady.” She fought back with two years of tax returns and won $20,000.

- Insurance Denials: Companies might claim you’re “fine” or could’ve worked sooner. Get detailed medical reports to shut that down.

- Future Loss Disputes: Proving loss of potential income takes expertise. Insurance companies love to argue you’ll “bounce back.” Experts can prove otherwise.

- California’s Comparative Fault: If you’re partly at fault (say, 20%), your wage loss compensation could be reduced by that percentage. Know your case inside out.

Keep every receipt, doctor’s note, and paycheck stub. And don’t go it alone—legal pros can navigate these traps like nobody’s business.

FAQs

1. How do I prove my loss of wages when I’m barely keeping my head above water?

You’re staring at a stack of bills, heart racing, wondering how to prove your loss of wages when you’re already stretched thin. It’s overwhelming, I know. Here’s the good news: you just need solid evidence. Grab your pay stubs, tax returns, or a letter from your boss showing what you earned before the injury. If you’re a freelancer, dig up invoices or app records, like DoorDash logs.

2. What does loss of income insurance provide when I’m out of work and stressed out?

You’re sidelined, bills are piling up, and you’re hoping loss of income insurance is your lifeline. But it’s confusing, and you’re scared it won’t cover enough to keep you afloat. So, what does loss of income insurance provide? It’s supposed to replace part of your income—maybe 60% of your salary—but policies are tricky. Some cap payouts at $1,000 a month or skip overtime and bonuses.

3. Can I claim wage loss compensation if I’m dragging myself to part-time work?

You’re pushing through pain to work part-time, exhausted and frustrated, wondering if you can still claim wage loss compensation. Here’s the deal: you can absolutely claim the difference between your full-time pay and what you’re scraping by with now. If you were earning $4,000 a month full-time but only $2,000 part-time, that $2,000 gap is your wages lost. Document your hours and pay stubs, and you’ve got a solid case for a loss of earnings claim. You’re fighting hard, make sure you get what you deserve.

4. What’s involved in suing for loss of potential income? I’m scared about my future.

You had big dreams, a promotion, maybe your own business, and now an injury’s got you worried that those are gone forever. Suing for loss of potential income is about fighting for the career you were building. It covers earnings you can’t make because your injury limits you long-term. You’ll need medical records, pay stubs, and maybe a vocational expert to show how your career’s been derailed. It’s a big step, but it’s your future on the line.

5. How long do I have to file a loss of earnings claim in California? I’m overwhelmed.

You’re juggling doctor visits, bills, and pain, and you’re terrified you’ll miss your chance to claim loss of earnings. In California, you’ve got two years from the injury date to file a personal injury lawsuit, including a loss of earnings claim. That’s the statute of limitations, and it’s a hard deadline.

6. I’m a freelancer with no steady paycheck. How do I prove my loss of earnings?

You’re hustling as a freelancer, and an injury’s got you stuck, panicking about how to prove your loss of earnings without a regular paycheck. It’s tough, but you’ve got this. Pull together tax returns, 1099s, invoices, or even Venmo payments from clients. Keep every financial record you can, as it’s your ticket to a fair payout.

7. What if my loss of income insurance claim gets denied? I’m so frustrated!

You’re counting on loss of income insurance to cover your wages lost, and then—wham!—they deny your claim. It feels like a punch in the gut when you’re already down. Denials happen for reasons like “not enough proof” or “policy exclusions.” Don’t give up. Check what loss of income insurance provides in your policy, then gather more evidence, like medical reports proving you can’t work. If they’re playing hardball, a lawyer can help you fight back.

8. I’m partly at fault for the accident. Can I still claim wage loss compensation?

You’re kicking yourself, wondering if a mistake you made means you’re out of luck for wage loss compensation. It’s a heavyweight, but here’s the truth: California’s comparative fault law says you can still claim, even if you’re partly to blame. If you’re 20% at fault, your payout might drop by 20%, but you’re not shut out. Don’t let guilt stop you from fighting for what’s fair.

Take Back Your Future

You’ve got the tools to tackle loss of wages, figure out what loss of income insurance provides, and build a bulletproof loss of earnings claim. Whether you’re dealing with wages lost or thinking about suing for loss of potential income, you don’t have to let an injury define your future. California’s two-year statute of limitations means time’s ticking, so don’t wait.

The emotional toll? It’s real. Missing work, worrying about bills, feeling like your dreams are slipping away—that’s heavy. But you’re not alone. Joseph Pluta Law At Attorney is here to fight for every dollar you deserve. Reach out for a free consultation, and let’s turn this setback into a comeback. What’s your next move? Make it a bold one.